Secure Access Services Edge Market Trends, Share & Forecast to 2035

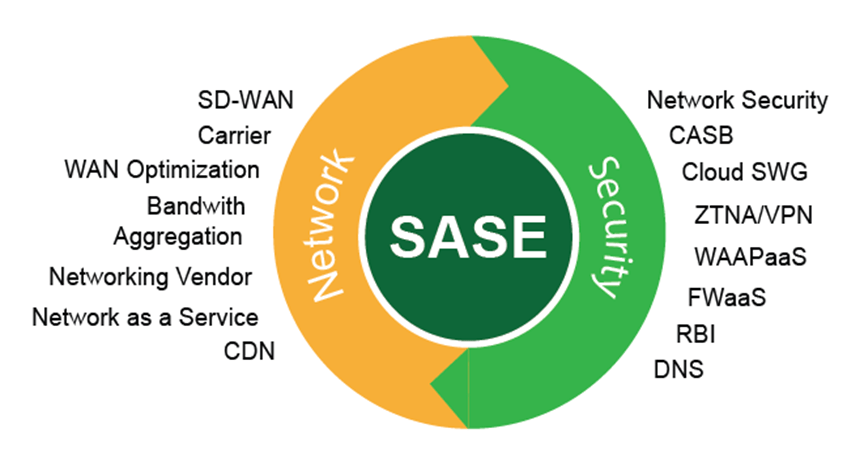

A comprehensive Secure Access Services Edge Industry Analysis reveals a fascinating and highly competitive industry born from the convergence of two distinct technological lineages: the network security world and the wide-area networking (WAN) world. This dual origin story is the single most important factor in understanding the industry's structure and the different competitive philosophies of its major players. The first group, often referred to as the "security-first" vendors, includes established cybersecurity giants like Palo Alto Networks, Fortinet, and Zscaler. These companies have their roots in building best-in-class security technologies like next-generation firewalls, secure web gateways, and cloud access security brokers. Their approach to SASE has been to take their powerful security stacks, re-architect them for a cloud-native, globally distributed delivery model, and then integrate or add the necessary SD-WAN networking capabilities. Their core value proposition is built on the strength, depth, and proven efficacy of their security services, arguing that world-class security is the most critical component of the SASE framework.

The second group, the "networking-first" vendors, emerged from the Software-Defined WAN (SD-WAN) space. Companies like Cato Networks and VMware (through its VeloCloud acquisition) built their businesses on revolutionizing enterprise networking, providing a more agile and cost-effective alternative to traditional MPLS networks. Their approach to SASE has been to start with a powerful, often private, global network backbone and a sophisticated SD-WAN fabric, and then to layer a comprehensive suite of security services on top of this network foundation. Their core value proposition is built on superior network performance, reliability, and the operational simplicity of having a single, unified platform that was designed from the ground up to be a converged networking and security solution. This creates a clear strategic choice for enterprise buyers: do they prioritize the "best-of-breed" security stack from a security-native vendor, or the integrated architecture and network performance of a networking-native vendor? This fundamental dichotomy is the central drama of the SASE industry.

A critical component of the industry's structure, and a massive barrier to entry, is the need for a global network of Points of Presence (PoPs). A SASE architecture functions by directing all user and branch office traffic to the nearest cloud PoP for security inspection and policy enforcement. The performance of the solution and the quality of the end-user experience are therefore directly dependent on the number, geographic distribution, and performance of these PoPs. The leading SASE vendors have invested hundreds of millions of dollars in building out their own global networks, with dozens or even hundreds of PoPs in data centers around the world, often with direct, high-speed peering connections to the major cloud and SaaS providers. This physical infrastructure is a formidable competitive moat. It is simply not possible for a new startup to enter the market and instantly replicate this global cloud footprint. This infrastructure requirement is a major reason why the SASE market is rapidly consolidating around a handful of large, well-capitalized platform players. The Secure Access Services Edge Market size is projected to grow to USD 42.86 Billion by 2035, exhibiting a CAGR of 22.1% during the forecast period 2025-2035.

Top Trending Reports -

Europe Application Performance Management Market